The Impact Capital Conundrum

Why is it that ever more capital is dedicated to creating impact, and yet not enough of it is reaching innovative fund managers and entrepreneurs?

As I round the corner to my 10 year anniversary of becoming a founder of a tech for good company, I have been reflecting on one thing:

NONE of the statistics I care about have appreciably changed in the last decade.

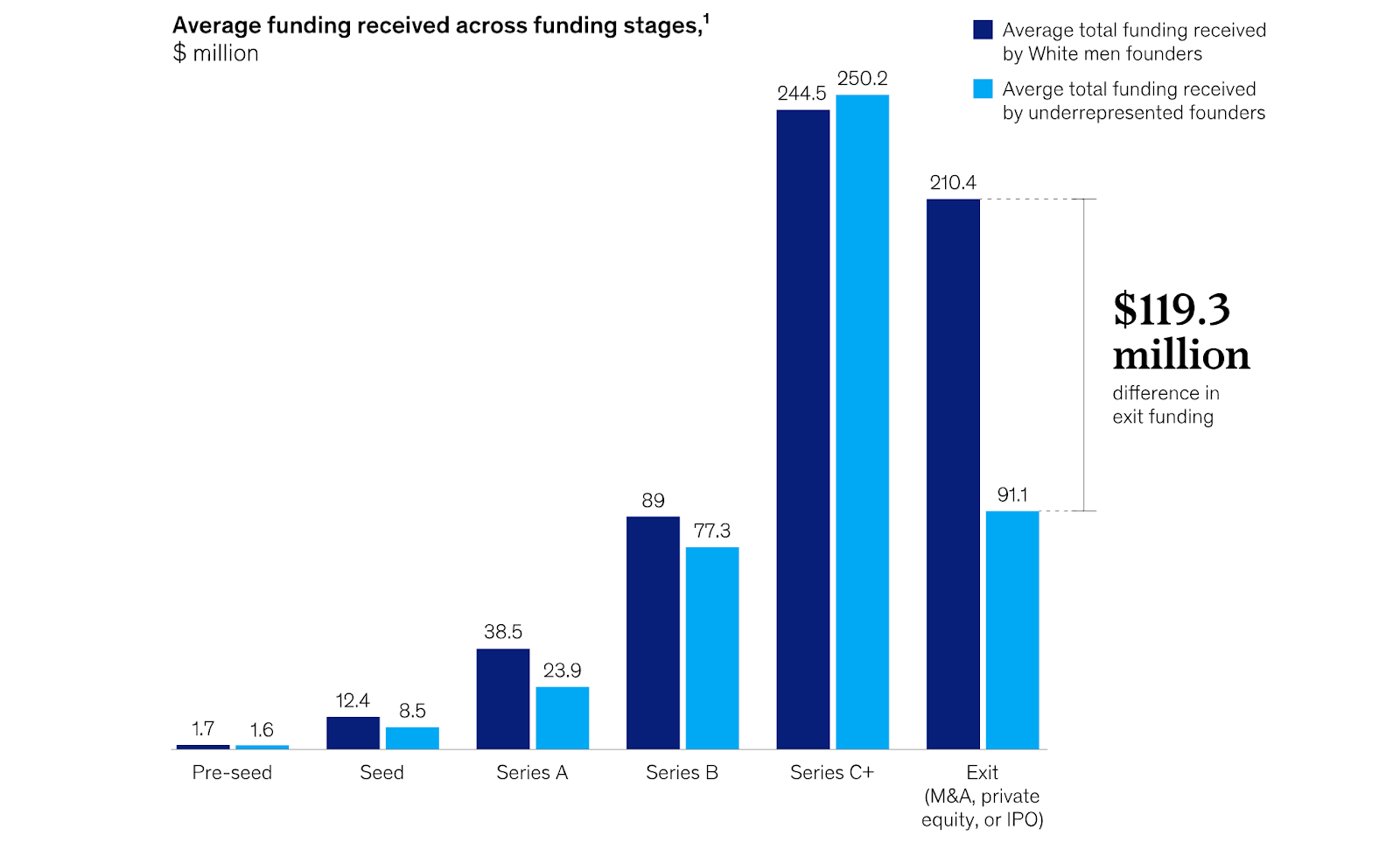

Women founders like me still only receive 2% of venture capital, people of color even less. 2024 is shaping up to be a new low, with Black founders receiving a mere 0.3% of the nearly $80 Billion of venture capital that flowed to start ups in the first half of the year. The money just isn’t moving at the volume and velocity we need. This massive capital access problem persists at every stage of a company’s life all the way to exit, according to a recent McKinsey & CO report:

Let that sink in: even if an underestimated founder succeeds against the odds to attract funding, on exiting, they are not creating the wealth for themselves that white men do. And, as the McKinsey report helpfully observes:

“It’s also a gap on both sides of the table—only 1.4 percent of the $82 trillion in US assets under management (AUM) is managed by women or BIPOC managers (as of 2021). In general, funds that flow from asset managers match their demographics.”

It was a sober message to deliver to an audience of incredibly talented, motivated and ambitious entrepreneurs at Sloss Tech in Birmingham, AL in June of 2024. While there is an encouraging local investing scene there, the demand for early stage funding way outstrips the local supply, and entrepreneurs in places away from the coasts like Birmingham, AL continue to face the same seemingly insurmountable odds as they did 10 years ago.

And it’s even worse if you are working on any kind of “social purpose” type venture. It’s a little depressing, at my age, to realize that today’s 20 and 30 year old entrepreneurs are launching themselves into this incredibly challenging fundraising environment with the same passion as we did when we were their age, knowing what I know now: the odds are still very much not in their favor.

Innovative finance to the rescue!

So what if venture capital is still systematically stacked against women and founders of color, surely there are alternatives these underestimated founders could tap into?

Indeed there are! Thanks to Jamie Finney and Aunnie Patton Power we have a grammar and playbook for understanding alternatives to venture capital as a source of finance for ambitious and impact minded entrepreneurs. These are real resources for how to approach revenue based and other financing options, how to structure them, what terms to create, and how to drive those conversations as both entrepreneurs and investors.

Furthermore, there has been an encouraging amount of experimentation with those alternatives to venture, and there is a growing number of capital innovators who are building investment funds that are using revenue based strategies, debt, mezzanine structures, real estate, and micro PE to invest in businesses and create wealth in underserved communities like Birmingham, AL.

By all accounts, revenue-based finance writ large is growing globally, and is beginning to turn into a recognizable asset class. There have been some great programs, like the Capital Access Lab of the Kauffman Foundation that invested in the managers of innovative investment funds that were using revenue-based strategies to invest in underestimated founders. Investing in the managers of revenue based investment funds, the Kauffman initiative aimed to promote the growth of emerging funds and create more supply of founder-friendly capital. Typically these were investments of $500,000 into first time funds that were each raising between $5 and $20 million. Not a huge amount of new capital unlocked, but better than a poke in the eye with a sharp stick.

The progress of revenue based finance is an encouraging signal, and it’s worth quoting a recent overview article at length:

“RBF can be structured as a redeemable equity investment, in which the company buys back the investor’s equity as revenue grows over time, or as a revenue-based loan. In either case, an RBF recipient repays the investment as a share of their revenue, typically 2-5%, until an agreed-upon multiple or cap of the principal amount, typically 1.4-2x, is reached.

RBF provides much-needed flexibility for borrowers and investees by tying repayments to cash flows. Moreover, its underwriting is less reliant on existing asset bases for collateral than traditional lending, making it accessible for asset-light businesses. And with an investment exit built into its structure from the beginning via revenue-based repayments, it provides an alternative to the endless march toward higher valuations and an eventual sale required by venture capital.”

Not so fast…

At a gathering hosted by the Kauffman Foundation in early 2020, however, I discovered this incongruity: in talking with the foundation’s chief investment officer, she revealed that the investment side of the house could not participate directly in the Capital Access Lab because she is not able to write checks smaller than 1% of the corpus, or $25 million at the time, given the then size of the total assets under management for the $2.5 billion foundation. Further, she was not allowed to take more than a 10% position in any one fund they invest in. In short, the SMALLEST fund she could invest in was a $250 million fund. At the time, there was no such thing in revenue based finance, and 5 years later I am aware of only a few funds that might fit this bill.

This is not to throw shade on the Kauffman Foundation. They are not the first or last foundation to get caught in the “two pocket problem” – where grant funded initiatives like the Capital Access Lab cannot be fully supported by the investment side of the house due to the constraints of the governing documents and internal rules. If we solved that two-pocket problem and aligned 100% of foundations’ assets with their mission, this could unlock the $1.8 Trillion sitting on US foundations’ balance sheets alone. The Kauffman Foundation dilemma is just a symptom of the structural problem we are facing: the innovative finance vehicles that we need to drive capital to underestimated founders and communities are not maturing quickly enough to absorb the institutional capital that is hamstrung by its internal investment rules. Another way to look at this is that allocators just aren’t getting off their assets quickly enough, and are not rising to the opportunity presented by these innovative emergent fund managers. But more on that in the next section.

So while it is true, that there is now $1.6 Trillion deployed for impact globally, as per the latest GIIN report, it also remains true that the plumbing does not (yet) exist to drive this capital to the most innovative emerging fund managers. Thus, nor does it reach the entrepreneurs they serve. Foundations and family offices that, in theory, should and could be first in line to accelerate innovative finance, are blocked by their own internal logic.

A list of 67 impact funds that were raising in 2024 reviewed by ImpactAlpha, “disclosed about $1.1 billion in commitments against a target of $6.6 billion. First-time fund managers have secured about 30% of those commitments against a goal of $2.9 billion.”

Where are the impact investors?

It’s worth restating the McKinsey & Co insight from above, that “funds that flow from asset managers match their demographics.” In other words, women fund managers invest in women, BIPOC managers in BIPOC entrepreneurs, and so on. If shared lived experience is key to assessing a business idea, white men are reliably investing in white men and the things white men are interested in. I am going to generalize this statement a bit more, and postulate that fund managers who have direct, lived experience with any number of social, economic, and / or environmental issues create innovative vehicles and investment theses informed by those experiences. That’s why, for example, the majority of the members of the Inclusive Capital Collective are employing innovative debt, equity and / or real estate strategies to not just create wealth for themselves and their investors, but their communities too. This takes the form, for example, of community owned commercial or mixed use real estate. Or funds that make equity-like investments in early stage businesses but take debt-like repayment on non-extractive terms. Whomever has the capital under management will drive the outcomes on the ground. And only 2% of all assets are managed by women and people of color.

Investing in more diverse fund managers and innovative investment theses could be hugely catalytic in terms of changing the outcomes we want. For me, these outcomes all fall under the rubric of the Sustainable Development Goals articulated by the United Nations for ensuring a thriving planet for all. In theory, impact investors could play a leading role in achieving the outcomes we want by directing capital into these innovative vehicles.

We put that theory to the test at SOCAP24, where my company Armillaria partnered with three other members of the Inclusive Capital Collective–New Majority Capital, Roanhorse Consulting and Common Future–to host the Inclusive Capital Exchange. Inspired by the deal rooms that are part of mainstream finance conferences, we invited emerging fund managers who are currently raising funds 1, 2, or 3 and investors who are currently deploying capital into funds to fill out a short form to tell us what they were looking for. We were able to match 7 investors with 42 fund managers (out of over 140 who applied to be there) at an in-person event during SOCAP, and we will be following up to see how much capital flowed as a result.

We asked the investors to confirm that they are in fact able and willing to write checks by the end of the first quarter of 2025, and that simple question to ensure we are not wasting the fund managers’ time was apparently off-putting to some folks. The impact space is famous for people taking a very long time to make investments, and for expecting to be treated with deference to their quirks, theories of change, and frequently confused thinking about financial returns, risk profiles, and measurable impact. We are keeping our fingers crossed that this first Inclusive Capital Exchange will move some real capital, and also plan to host future Exchanges at impact conferences where impact investors, fund managers and entrepreneurs gather.

Reasons for hope

While the Inclusive Capital Exchange experiment plays out, there are some reasons to hope that 2025 could be a turning point for figuring out the impact capital conundrum. And I don’t mean the noise pollution that is the AI hype. Like so many silver bullets and hype technologies before it, AI will not fix this. But that’s a topic for another post.

Instead, what is encouraging to me as we go into 2025 are a number of emerging trends and patterns that I am sensing.

First among them, the rallying cry of systemic investing for social change, a new investment logic that applies systems and complexity thinking to investing and is being embraced by an increasing number of family offices, foundations and private investors. The cynic in me is quick to point out that systemic investing and its cousin, bioregional finance, are new words for old ideas that are long on concepts and intellectual frameworks, and short on actual financing facilities. The impatient pragmatist in me, however, sees this as a welcome sea change in impact investing, which has been notoriously fragmented and has been characterized by overly specific geographic and / or sectoral investment theses rather than taking more integrated approaches to investing in change.

Another welcome development, for the first time in my 10 years building an impact tech company, there appears to be interest from impact investors in underwriting infrastructure technology designed for mobilizing capital, innovations and people for impact. Not in the sense of electronic wallets or other last mile finance solutions, but workhorse technology that makes it easy and efficient to source impact deals, do and share diligence, syndicate, underwrite, monitor and aggregate outcomes across portfolios and investors. Our 2018 report on the missing impact finance infrastructure finally has several family offices actively investigating the issues diagnosed, I am hopeful that we will see real progress this year in data liquidity, interoperability, sovereignty and agency. Incidentally, these are all prerequisites for an eventual ethical deployment of AI for impact finance.

Looking to disrupt the “wealth defense industry” from within, the Wealth Hackers Initiative takes on the very tools, protocols, and behaviors that keep wealth locked up for the few at the expense of people and the planet. The idea is to work with accountants, lawyers, intermediaries, financial modellers and others to create the new tools, norms and practices that align wealth management with the values of the next generation(s) of private wealth holders while we go through what’s been called the greatest wealth transfer - over $80 Trillion passing from the Baby Boomer to their millennial and Gen X heirs. Remember the internal rules of the Kauffman Foundation? Those are the kinds of things that need to be broken and reimagined, and I am looking forward to the first six hacks that we are funding and meeting the intrepid wealth holders who’ll put them to work.

And last, but not least, the Innovative Finance Initiative is an exciting new effort sponsored by The Impact, which is sort of a family office of family offices. The IFI takes an ecosystem approach to popularizing innovative finance structures, creating a community of practice around them, and developing the infrastructure for making it easy and delightful for wealth holders to not just learn with and from each other, but combine and channel their capital to maximum effect. During the soft launch of the initiative in December, I was encouraged by the networks and organizations represented and their commitment to get practical and tactical with each other.

Whether you learn about systemic investing for your own investing practice, or get involved with one or more of the mentioned initiatives and projects, I hope you’ll be part of the push in 2025 to solve the impact capital conundrum.

Innovative Finance Announcements

| A guest post by

|

Excellent points Dr. Astrid Scholz. I also think that the systemic and bioregional approaches to impact investing have the potential to change the game - so long as they go all the way.

Which means no longer using portfolio theory to structure investments.

The expectation value and risk thinking that portfolios are built around is itself a very little known root cause of the challenge impact investing has, including much else that you point out in your article. If typical outcomes are far from average, which happens in any complex system, you know that the statistics being used are failing to describe reality! Instead you need to use the far more difficult statistics of non-ergodic complex systems.

A 1m and 10m video of this, and lots more in my book The Ergodic Investor and Entrepreneur, and in our offerings on systemic investment for investors at Evolutesix.

1m: Can impact investing do better? https://youtube.com/shorts/g8fUiIttLis

10m: Yes it can: systemic ergodic impact investing: https://youtu.be/mRehLtOvRx4

Btw, herds of Zebras can solve this problem! I draw the links in this interview with Carsten Terp of Impact Insider : https://impactinsider.dk/graham-boyd-stop-chasing-unicorns-zebras-create-more-value/